Which is a better investment in 2025: ISA or Gold?

What are the tax benefits of ISAs compared to gold?

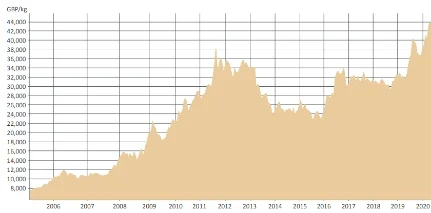

How have ISAs performed compared to gold over the last 10 years?

Should I invest in both an ISA and gold?

Gold vs other assets

Silver Investment

Sources, supply and demand

“You should think of gold as being a fundamental money that you should own at least some of. Most investors...

The Best Gold Investors Do These 5 Things So, here we are. Gold at £3000. Fancy seeing you here. Gold...

On Wednesday morning, gold hit a new all-time record high of £3000 ($4000) as a wider range of investors...

Last week, the investment bank Goldman Sachs issued a note predicting gold could hit $5000 (£3700) if...

Gold Hits Yet Another High. Can It Go Higher? On Tuesday, gold hit a new record high surpassing £2,600...

In 2025, many of us rely on AI for a wide range of tasks. Some of us use it for quick facts like “When...

What is inflation? Inflation refers to the rise in price for goods and services. In June, UK inflation...

To me, gold has always had a unique and fascinating relationship with humans ever since the very first...

What makes gold so attractive to investors, countries, and those simply looking to protect their wealth...

Imagine you are in government and you want people to buy more Aston Martins (let’s just say for argument’s...