Would you, for example, put a tax on tractors in order to get more people to buy Aston Martins? You are increasing the price of one vehicle in the hopes that people will bin off their tractors to buy the luxury car brand.

If you answered: “God no, what a stupid thing to do” then you might have the same reaction to the changes coming to the Cash Isa.

The chancellor, Rachel Reeves, wants to cut the tax-free allowance on Cash Isas so that savers put more money into UK stocks. The current limit that savers can put into Cash Isas is £20,000 per tax year. Individuals then earn tax-free interest on this money. This figure is set to be reduced on the 15th July at the chancellor’s Mansion House speech. Although it is yet to be confirmed, the figure is reported to be as low as £5,000.

I personally have a few issues with this policy. Following the example I gave at the beginning of this piece, the Cash Isa is the tractor. Like a tractor, the Cash Isa serves a specific purpose. It helps those who want to see their money grow incrementally at a low-risk, they may be saving up for a life event such as for a wedding or a house, or they are simply unfamiliar with stock investing and uncomfortable with their money in higher risk profile positions. If the goal then is to encourage more people to invest in UK stocks, I don’t see how cutting the Cash Isa is the answer. Even if the government wishes to target younger people to invest in stocks because they historically yield a better return over time, a survey conducted by St James’s Place found that 1 in 2 young adults were delaying “major life milestones” due to a shortage in cash. This implies to me that young adults don’t have large positions in stocks either if they need every penny to survive.

Cash Isas and UK stocks serve totally different purposes. Just like how a tractor is used for farming, an Aston Martin is of no use to a farmer who needs to look after his land. Similarly, changing the incentives to save does not tackle the reason WHY people have money in a Cash Isa. They are not substitutes in the same way a snickers may be a substitute for a Kit Kat. Not to mention it is irresponsible for the government to potentially push people to make poor financial decisions.

Why is the government doing this?

Well, the government wants to make London an attractive stock market listing for companies. London recently hit a 30-year low in IPO fundraising and this Labour government wants to prove it is pro-growth. This will be, for all intents and purposes, an uphill battle since they have seemingly done their utmost to prove otherwise.

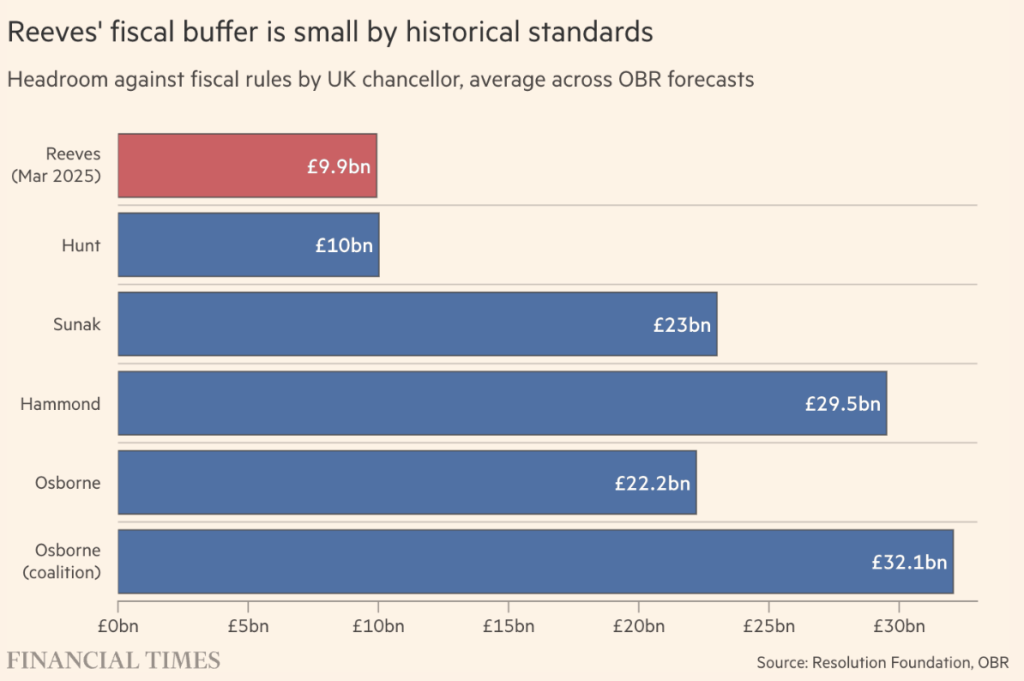

The other reason to make the Cash Isa changes is to increase tax revenue. With the U-turns on welfare reforms, a limping British economy and poor productivity growth, Rachel Reeves’ own fiscal rules are in danger. Productivity is important because the OBR calculates that just a 0.1 percentage point reduction in productivity growth would dissolve the chancellor’s £9.9bn fiscal headroom. When an economy doesn’t grow, more money for some means less money for another. Therefore, for those who continue to deposit money in a Cash Isa above the new threshold will now have to pay MORE tax. Given the U-turn on welfare reforms and increased borrowing costs, economists predict that taxes will be raised in the autumn Budget. Don’t all jump for joy at once.

Where does that leave me?

All this talk about snickers, KitKats, tractors, and Aston Martins have left me feeling hungry with James Bond-like neutrality.

More importantly, when we talk about substitutes for Cash Isas, gold comes to my mind.

What are some overlapping qualities between Cash Isas and gold coins?

- They’re both tax-efficient. Gold coins are Capital Gains Tax free and VAT free because they are legal tender. In fact, gold coins are more tax-efficient since there is no limit unlike the £20,000 limit in Cash Isas (soon to be less).

- They’re both considered to be lower risk ways of storing money. A Cash Isa is not totally risk-free. Under the FSCS, individuals are protected up to £85,000 if their bank or building society goes bust. Gold is known as the “safe haven” asset and although the price can go up and down, over the long term it has proven its worth as a great store of value. So much so, that central banks buy gold for their reserves (granted in quantities much vaster than you and I) because the precious metal is there for a rainy day and maintains its value against currencies.

- Most importantly – gold and Cash Isas are not stocks!

So when the changes do kick in on July 15th, it might be nice for us to have a think about how we can strengthen our financial futures in a way that is comfortable to us. If you wish to learn more about gold and its potential role in your life, please do get in touch with us.